By KURT DAVIS JR.

There are some simple life lessons in business: It is hard to be liked by all people and it is hard to be liked all the time.

Leaders at central banks and investment firms know this very well… today’s economic crisis will likely end with a simple reminder.

The Federal Reserve: Essential to Society or The Source of the Problem?

There are few, if any, central bankers who are not taking some public criticism today for raising rates.

For Jerome Powell, chairman of the Federal Reserve, and the other Fed members, their position cannot be enviable: stop inflation and maintain financial stability.

It is always a tough assignment to raise interest rates (the usual dose of…

By KIMBERLEY HAAS

Changes to fees for loans backed by Fannie Mae and Freddie Mac continue to be a hot topic as Republicans push to repeal them.

The changes to the loan-level price adjustment matrix by officials at the Federal Housing Finance Agency went into effect on May 1 and critics are opposed to the notion that homebuyers with good credit scores and substantial down payments will pay more so fees for borrowers limited by income or wealth can be reduced.

Rep. Warren Davidson, R-Ohio, who introduced the Middle Class Borrower Protection Act on Monday, again attacked the policy on Wednesday. He refers to it as “a socialist redistribution of wealth.” Biden’s mortgage fee is a socialist redistribution of wealth.…

By KIMBERLEY HAAS

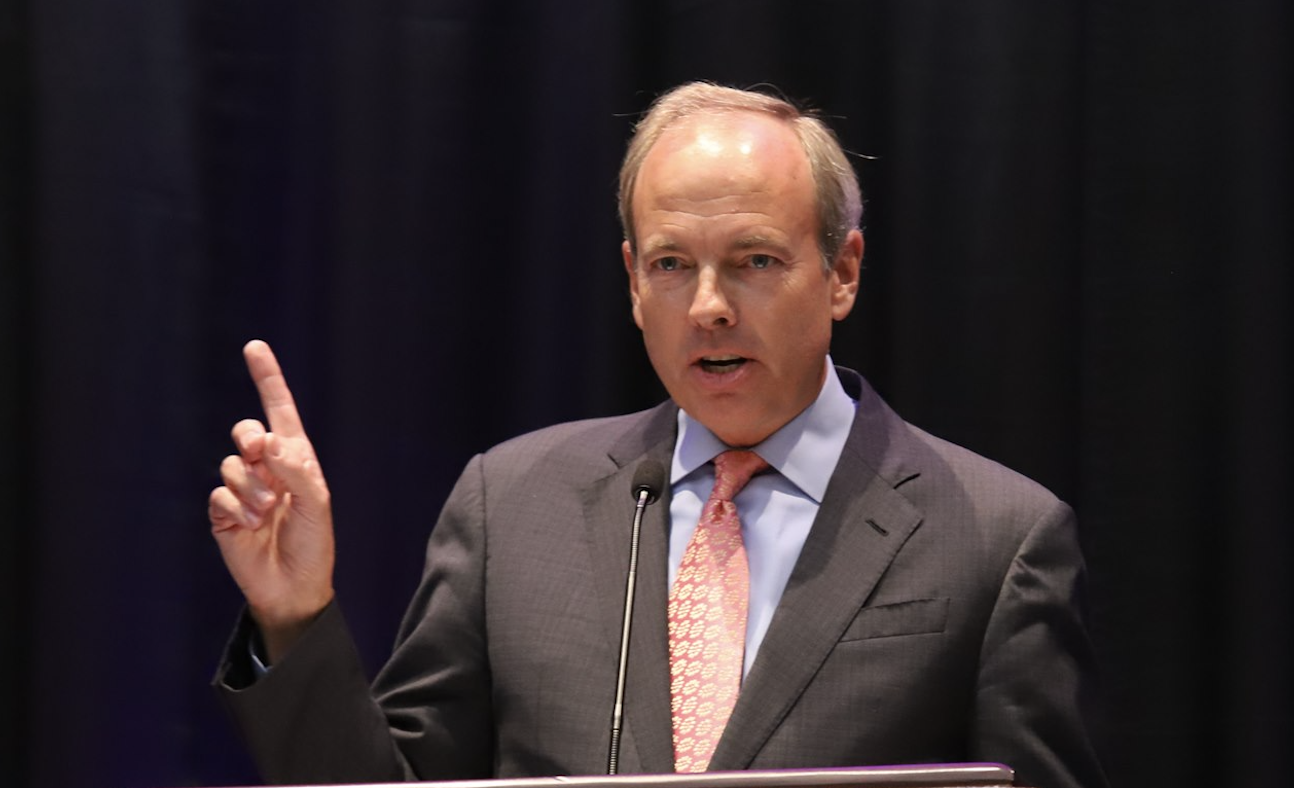

The president and CEO of the Mortgage Bankers Association said they are pushing for clarity and common sense as he criticized policymakers this week during his remarks at the Secondary and Capital Markets Conference and Expo in New York City.

Bob Broeksmit said policymakers plan to pile on more enforcement and red tape at a time when MBA member businesses are struggling.

“There seems to be a sense, at the highest levels of government, that the mortgage industry needs to be reined in,” Broeksmit said, according to his prepared remarks.

Broeksmit referred to the recent failures of Silicon Valley Bank, Signature Bank, and First Republic Bank saying some policymakers are now pushing for new rules that could…

By KIMBERLEY HAAS

A Virginia man who worked as an assistant inspector general for the U.S. Department of Housing and Urban Development has been sentenced to one year and one day in prison after being convicted of engaging in a scheme to steer government contracts to a personal friend.

Eghbal “Eddie” Saffarinia, 63, of Front Royal, was sentenced on Thursday, according to a press release issued by officials at the U.S. Department of Justice.

Saffarinia was employed by HUD-OIG from 2012 to 2017 and oversaw the Office of Information Technology. He was also the head of contracting activity, according to court paperwork.

Prosecutors claim tens of millions of dollars in government business was affected.

Saffarinia allegedly concealed material facts about…

The Federal Housing Finance Agency has rescinded a rule changing upfront fees based on borrowers’ debt-to-income ratios.

If it had gone through, the policy would have created an adjustment for DTIs higher than 40% that Fannie Mae and Freddie Mac would acquire.

Back in March, the agency delayed the implementation of these fees to talk it through with industry leaders, who largely opposed the move.

One major concern was that small lenders would be hindered by compliance: disclosure laws require lenders to alert borrowers of pricing throughout the application process, but a borrower’s income and expenses can change dramatically throughout the loan procedure, requiring an unmanageable compliance burden.

The Community Home Lenders Association argued against the adjustment at the time,…

As the country approaches D-Day for defaulting on its debts, analysts are breaking down the impact of such a scenario on the economy.

The Treasury Department said in January that the U.S. was close to its $31.4 trillion borrowing limit. As a result, it announced “extraordinary measures” to keep the government’s funding above water through spring.

Treasury Secretary Janet Yellen and other experts are now saying the U.S. could default on its debt as early as June in a worst-case scenario.

Dramatic as the news may be, it’s highly unlikely that Congress would actually allow a breach of the debt ceiling.

“While we have a highly polarized Congress negotiating, it isn’t in either party’s interest to let a default happen,”…

By CHUCK GREEN

Industry leaders and economists are sharing their opinions about changes to fees for loans backed by Fannie Mae and Freddie Mac after reports that homebuyers with good credit scores and substantial down payments will pay more so fees for borrowers limited by income or wealth can be reduced.

The changes to the loan-level price adjustment matrix by officials at the Federal Housing Finance Agency went into effect on May 1 and are the target of two bills in Congress.

Rep. Stephanie Bice of Oklahoma, vice chairwoman of the Republican Main Street Caucus, introduced the Free Market Mortgage Act. She said the changes will force homebuyers with good credit to pay more for their mortgages to subsidize loans…

Much has been made in recent weeks of loan level price adjustments made by the FHFA. Analysts have called the changes unfair, saying they subsidize borrowers with low credit scores by charging those with good credit more for their loans.

Finance officials from twenty-seven states sent a letter to President Biden him to stop this “unconscionable” policy, saying it would be a “disaster.”

Rep. Barry Loudermilk (R-GA) called it “President Biden’s mortgage socialism rule” in a tweet and claimed borrowers with good credit scores would “see a spike in your borrowing costs” to fund mortgages for others. President Biden’s mortgage socialism rule went into effect yesterday. This means, if you have a high credit score (680+), and have a FHFA…

By KIMBERLEY HAAS

The new vice president of public policy at Rocket Central says his goal is to increase opportunities for people who have historically had difficulties achieving home ownership because of a host of barriers.

Karan Kaul, a housing finance veteran who worked as a principal research associate in the Housing Finance Policy Center at the Urban Institute prior to joining Rocket, said that means focusing on first-time homebuyers, people of color, and low- to moderate-income borrowers.

In a recent interview with The Mortgage Note, Kaul said a well-documented hurdle to homeownership is a lack of an adequate down payment, especially with the increase in home prices over the last decade.

“So what can we do to make sure…

Officials at the Consumer Financial Protection Bureau have issued a reminder about zombie mortgages, saying threatening homeowners regarding uncollected time-barred debts violates the Fair Debt Collection Practices Act.

The guidance warns that it is illegal for debt collectors to threaten foreclosure on silent second mortgages with statutes of limitations that have expired.

“Some debt collectors, who sat silent for a decade, are now pursuing homeowners on zombie mortgages inflated with interest and fees,” said CFPB Director Rohit Chopra. “We are making clear that threatening to sue to collect on expired zombie mortgage debt is illegal.”

The CFPB points to “piggyback” mortgages in particular, also known as 80/20 loans. Homebuyers would be given a first lien loan for 80% of the…