The Consumer Financial Protection Bureau announced Monday a lawsuit against Fifth Third Bank for allegedly creating fake accounts on customers’ behalf to artificially inflate sales numbers. Fifth Third officials said in a news release that it “rejects” the allegations in the lawsuit. The CFPB said that for several years Fifth Third created accounts without consumers’ knowledge. For several years, the CFPB says, Fifth Third employees created fake credit card accounts, improperly transferred money into fraudulently opened accounts, enrolled customers in unauthorized online-banking services, and activated unauthorized lines of credit on consumers’ accounts. “Fifth Third Bank respects and values the important role that the CFPB plays in protecting consumers but believes that the civil suit filed today is unnecessary and unwarranted.…

House Financial Services Committee Chairwoman Maxine Waters expressed concern about the Federal Deposit Insurance Corporation’s plan to close offices and offer buyouts to 20 percent of its workforce. “I am deeply concerned by the FDIC’s decision to massively downsize its experienced workforce and close or consolidate offices in Los Angeles and across the nation,” Waters, D-California, said. “The FDIC should be working to ensure stability in the financial system, not to destabilize the livelihoods of its employees.” Last week, the FDIC announced it is offering voluntary retirement and early separation to as many as 1,200 employees. It also said several field offices will be closed and consolidated with other offices, including those in Oklahoma, Florida, Kentucky, Tennessee and Ohio. The…

The Federal Deposit Insurance Company (FDIC) announced Thursday that it is seeking to “reshape the agency’s workforce” by offering voluntary retirement and early separation to 20 percent of its employees. That could be as many as 1,200 employees. Additionally, the FDIC said several field offices will be closed and consolidated with other offices. The buyouts are not designed to reduce the FDIC budget or the overall size of the workforce, the FDIC said in a news release. Instead, it is seeking to rebalance the workforce by growing its examination and risk-related teams, while adding specialized information technology, computer science, data management and loan-review personnel. “Today’s announcement is part of a deliberate strategy to further reduce layers of management, acquire new…

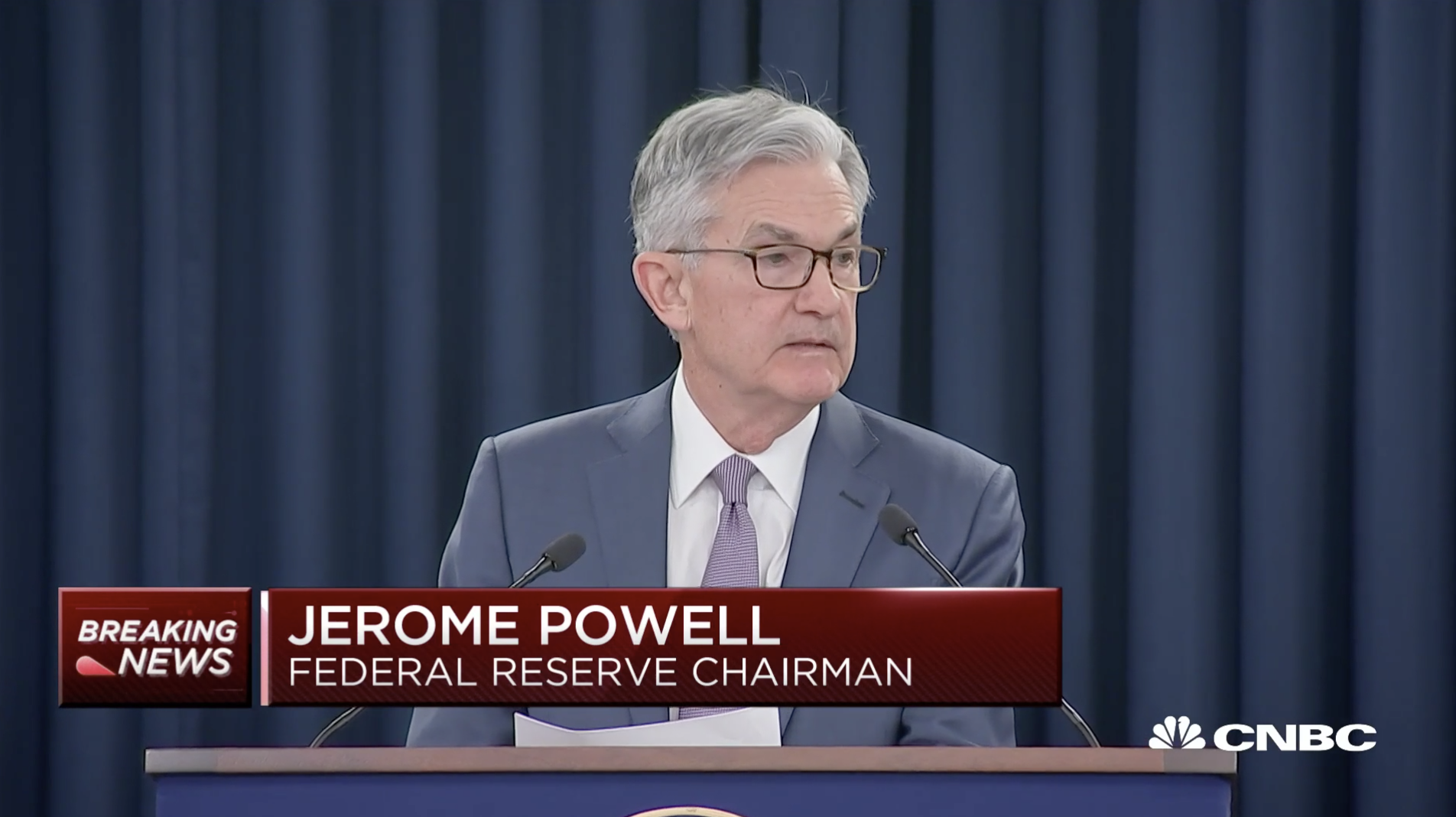

Brookings Institution Donald Kohn, a former vice chairman of the Federal Reserve, said on CNBC today that the Fed did the right thing by cutting interest rates this week. In the face of challenges posed by the coronavirus, Kohn said it is better for the Fed to be proactive – rather than waiting to react if the economy grows worse. Fed made ‘right choice’ on cutting rates, says ex-Fed vice chair from CNBC.…

CNBC provides a look at the impact the Federal Reserve’s rate cut is having on homebuilder stocks. Homebuilder stocks jump on news of a rate cut from CNBC.…

The Federal Reserve voted unanimously to cut interest rates on Tuesday in an attempt to head off economic damage caused by the coronavirus. It is the largest cut since 2008. Here’s a look at how people are reacting to the vote – and what they’re saying it means for homeowners. Dr. Lawrence Yun, Chief Economist at the National Association of Realtors, said: “The coronavirus has quickly upended global economic expansion and introduced the significant uncertainty of a possible recession. Today’s interest rate cut is therefore an appropriate response to changing events. The real estate sector will hold up very well because of the rate cut. Hesitant homebuyers will be enticed to take advantage of low interest rates. Commercial property prices…

Ahead of the South Carolina primary, former Vice President Joe Biden released a $640 billion housing plan that is designed to provide access to affordable, safe and energy-efficient homes that are “located near good schools and with a reasonable commute to their jobs.” Biden’s 5,200-word plan includes a refundable, advanceable tax credit of up to $15,000 for people buying their first homes; the creation of a $100 billion Affordable Housing Fund to build new and improve existing affordable housing; and ending “discriminatory and unfair practices” in the housing market. “Housing should be a right, not a privilege. Far too many Americans lack access to affordable and quality housing,” the Biden campaign said in announcing the plan. “Nationwide, we have a…

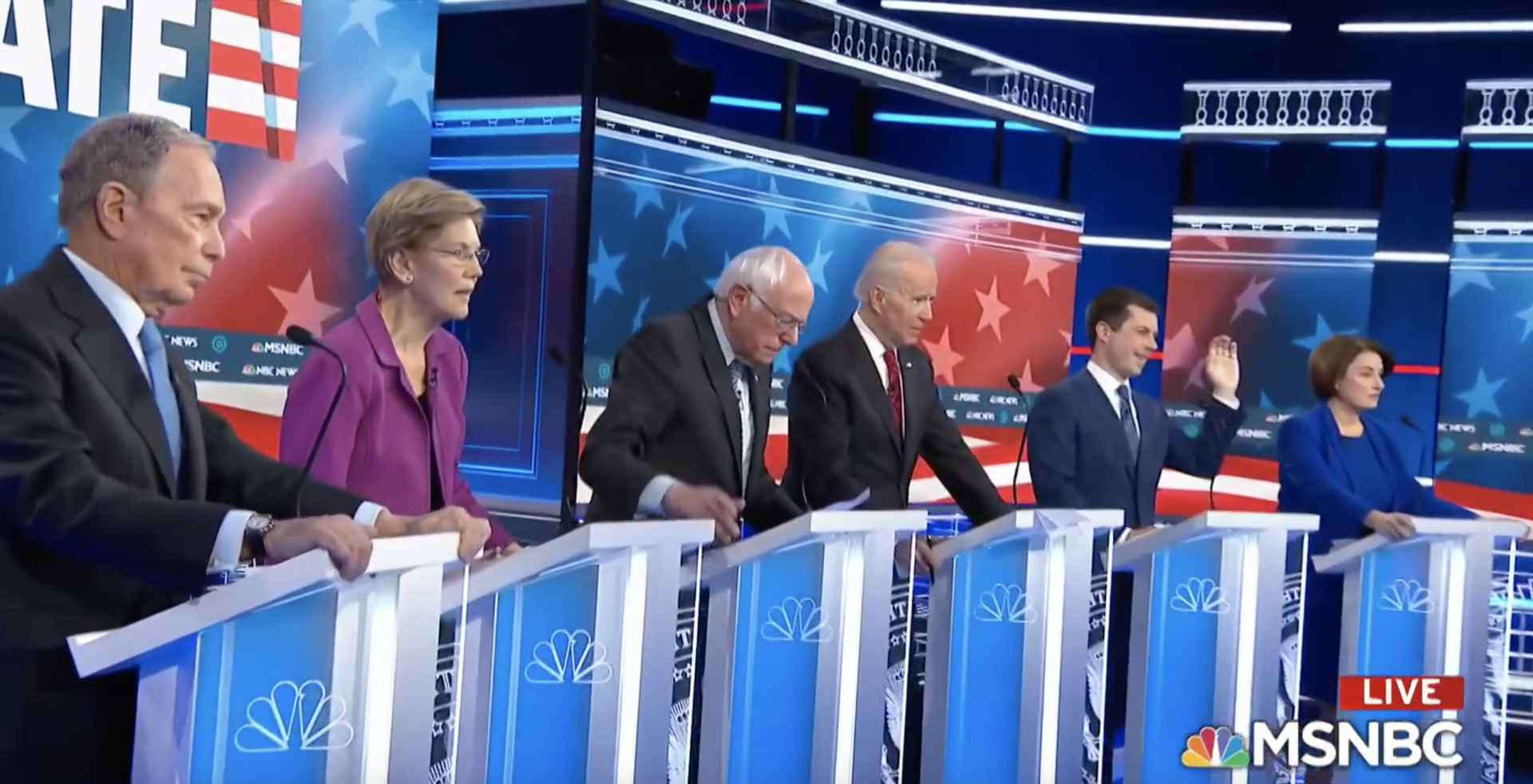

Housing was not a major – or even passing – area of focus in Wednesday night’s Democratic presidential debate in Las Vegas, though the issue of redlining came up a few times as candidates discussed tax policy and each other’s records. (Redlining is the practice of denying mortgages – or other goods or services – to whole neighborhoods on the basis of race or ethnicity. The Community Reinvestment Act of 1977 made all redlining practices illegal.) Here’s a look at what the candidates had to say on the issue: Senator Elizabeth Warren referred to former New York City Mayor Mike Bloomberg’s record, accusing him of supporting redlining in the past. SENATOR ELIZABETH WARREN: Democrats are not going to win if we have a…

With the release of the Federal Reserve’s minutes from its January meeting, economists told CNBC on Wednesday they expect interest rates to hold steady throughout the year, given the state of the economy and the fact that it is an election year. RBC Capital Markets economist Tom Porcelli and Kevin Caron of Washington Crossing appeared on “Power Lunch” to discuss interest rates. Watch below.…

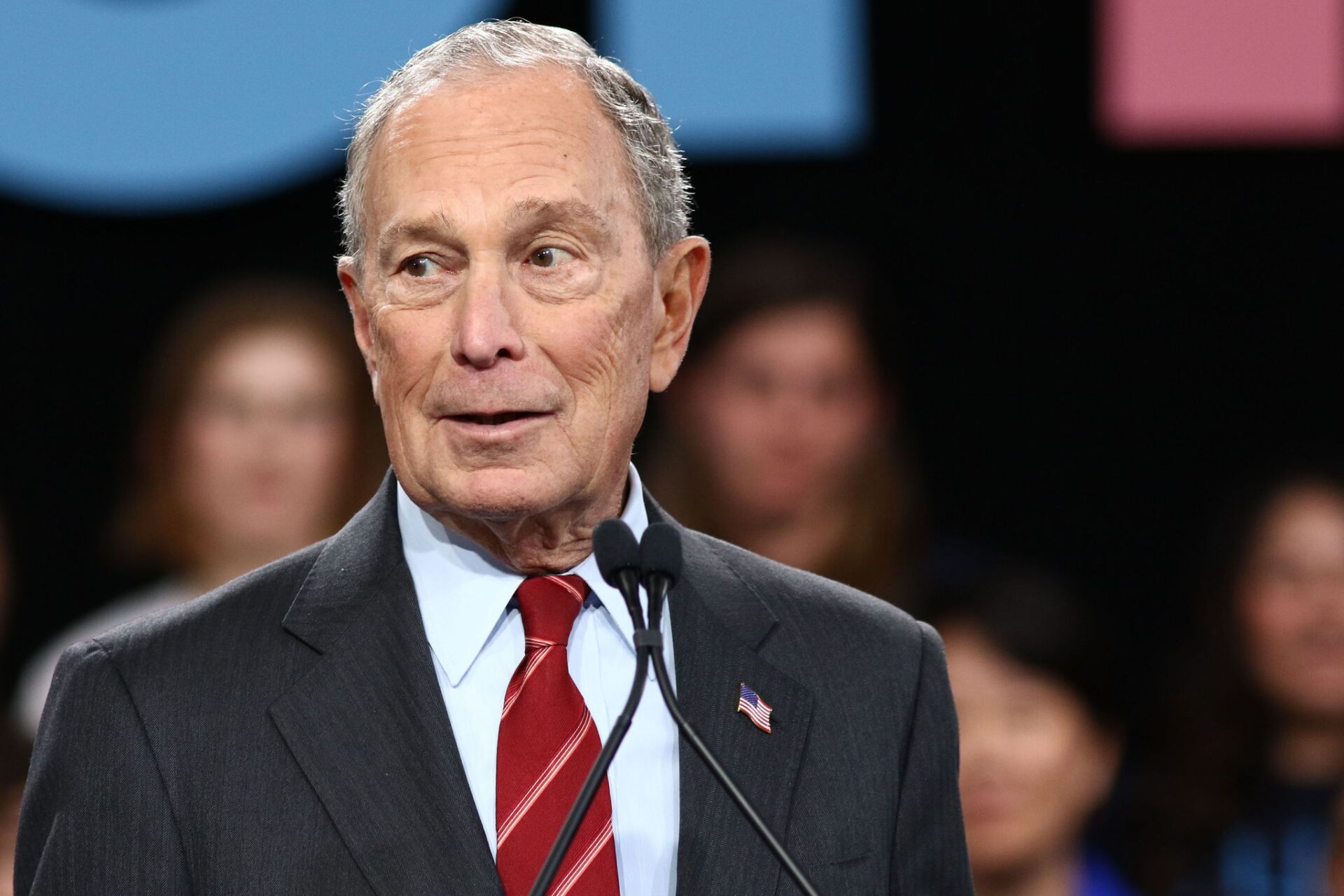

Democratic presidential candidate Mike Bloomberg announced Tuesday

he would merge Fannie Mae and Freddie Mac into a single government-owned

mortgage guarantor, as part of a larger package of initiatives “to reform Wall

Street and put the financial system to work for every American.” An announcement

from the Bloomberg campaign said merging Fannie and Freddie would “ensure

taxpayers are properly compensated for loan guarantees and low-income

households are well served.” Bloomberg said his plan would gradually merge Fannie and

Freddie into a single, fully government-owned mortgage guarantor, “to ensure

that taxpayers are fully compensated for the risks they are assuming – and that

lower-income households are well served.” The plan calls for the guarantor to transfer downside risk

to private investors…